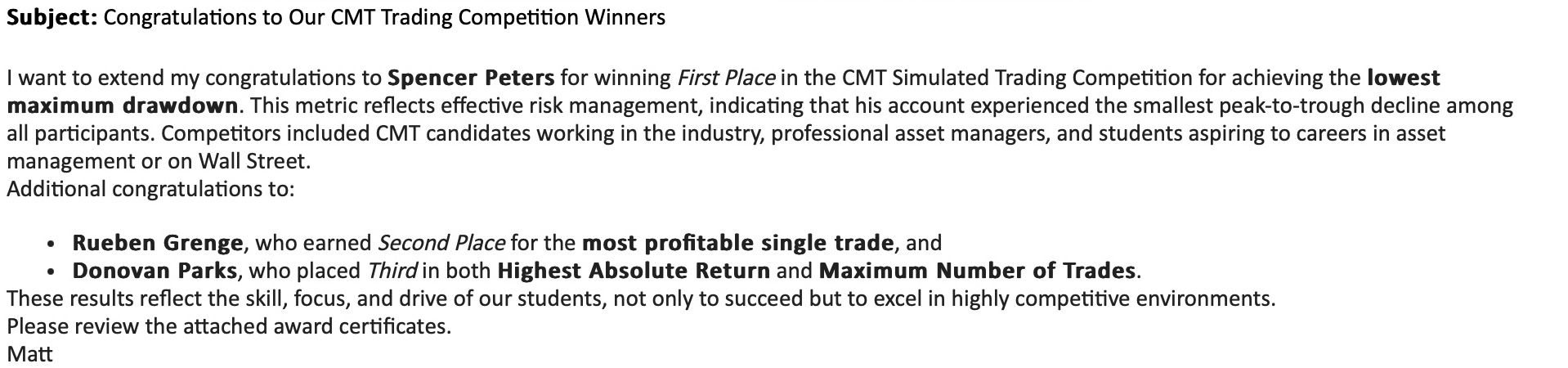

How CAN SLIM Is Used

The system is generally used as:

Step 1 — Screen for Candidates

Investors screen thousands of stocks using:

-

EPS growth,

-

sales growth,

-

RS ranking,

-

industry strength,

-

volume behavior,

-

new highs.

Step 2 — Analyze Charts

Technical analysis is heavily integrated.

Common concepts:

-

breakouts,

-

bases,

-

consolidation patterns,

-

volume confirmation,

-

moving averages.

CAN SLIM is NOT purely fundamental investing.

It is a hybrid:

Step 3 — Buy on Confirmation

Instead of buying falling stocks,

CAN SLIM investors usually buy:

-

breakouts,

-

strength,

-

confirmation moves.

This differs from traditional value investing.

Step 4 — Manage Risk

Sell rules are critical.

Typical rules:

Many implementations use:

Why CAN SLIM Became Popular

Historically, the framework identified many high-growth winners early in their advances.

Examples often associated with CAN SLIM-style traits:

-

Apple

-

NVIDIA

-

Amazon

-

Microsoft

before or during large institutional growth cycles.

Main Criticism of CAN SLIM

The strategy can:

-

underperform in sideways markets,

-

suffer during sharp reversals,

-

experience whipsaws,

-

buy “expensive-looking” stocks,

-

and rotate frequently.

That is why many modern implementations add:

-

tactical timing overlays,

-

macro filters,

-

moving averages,

-

relative strength filters,

-

or volume indicators.

For example, your own research emphasis using:

is essentially an attempt to improve the original CAN SLIM framework’s:

-

risk management,

-

market timing,

-

and drawdown control.

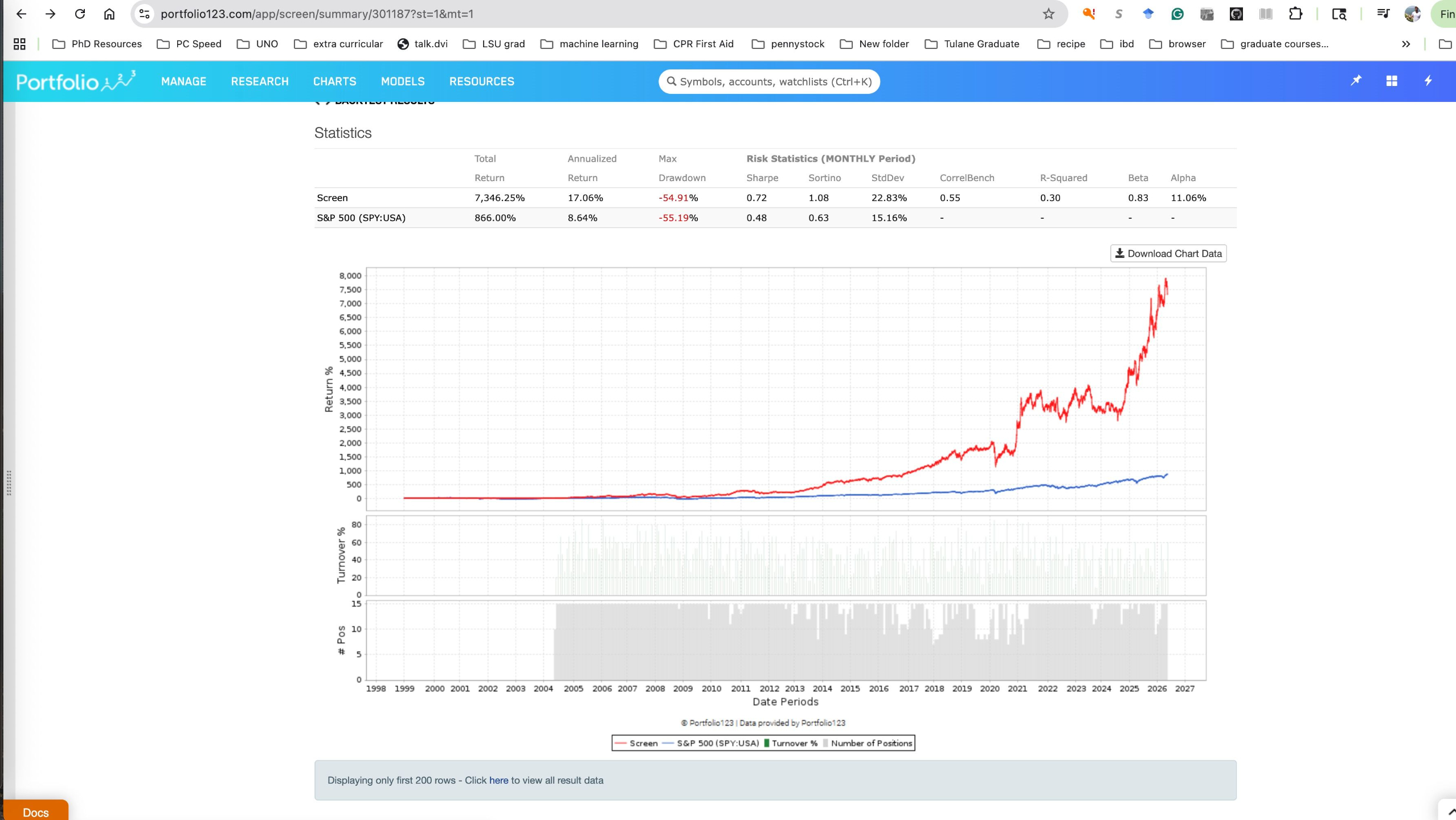

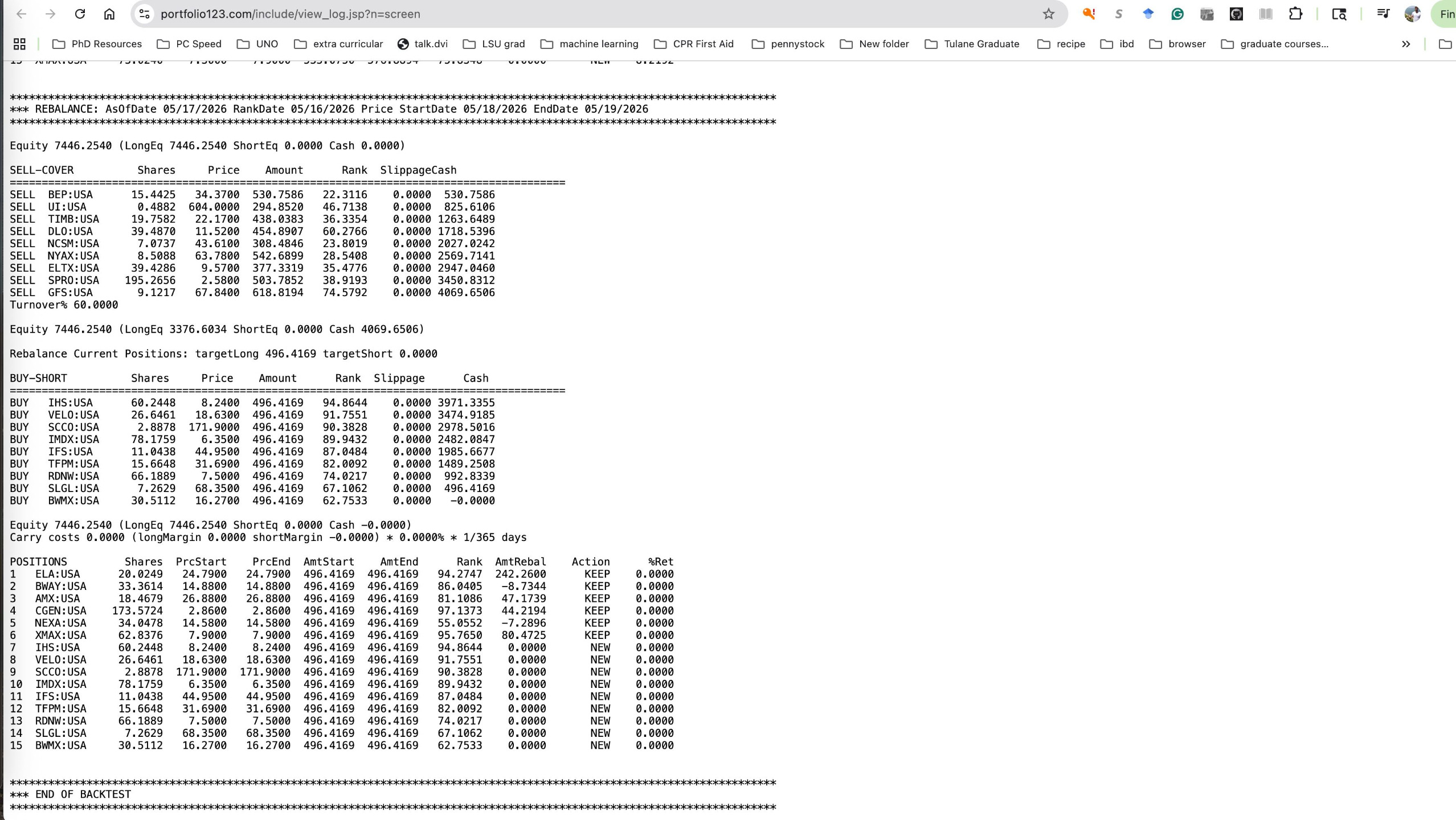

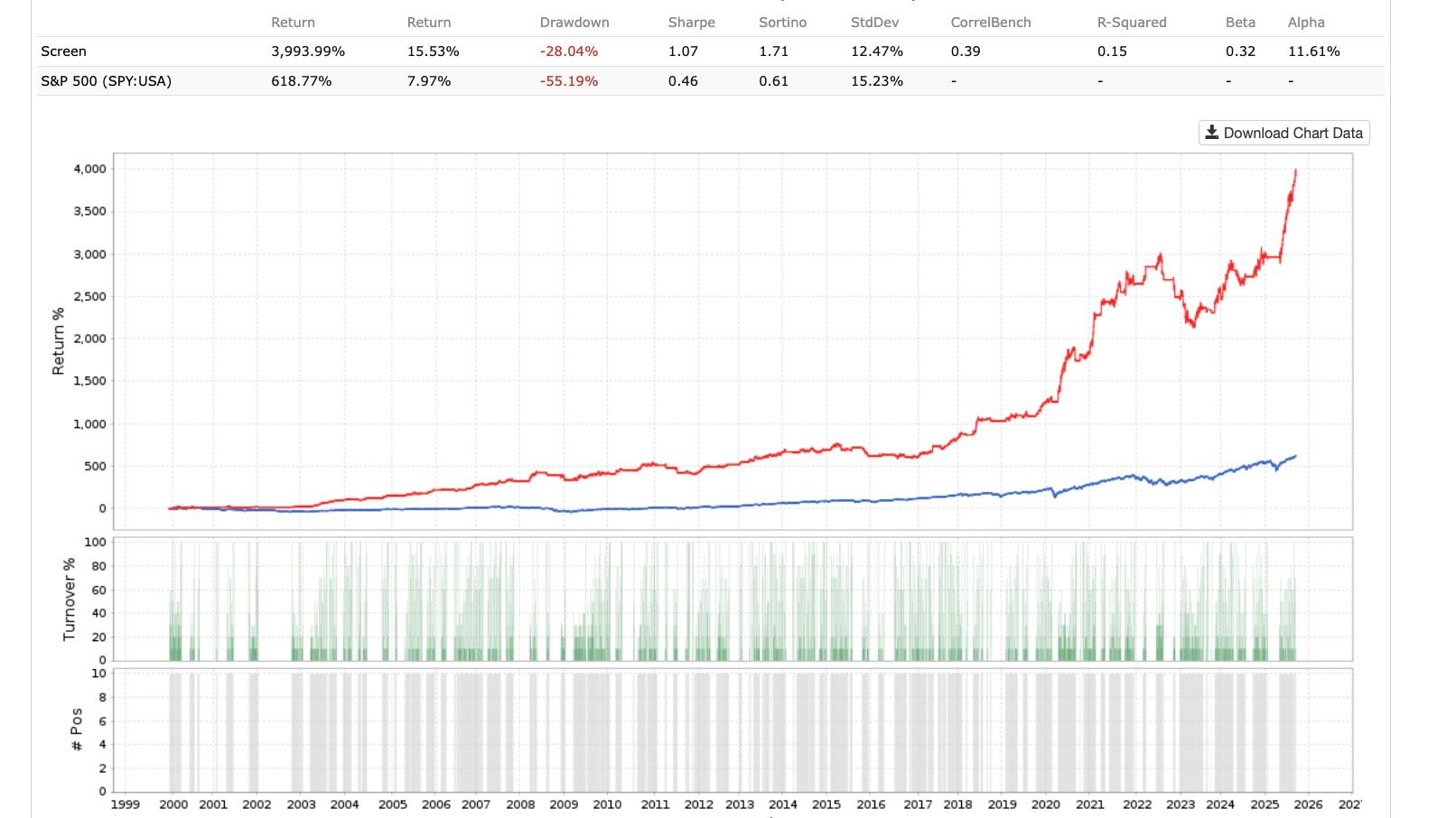

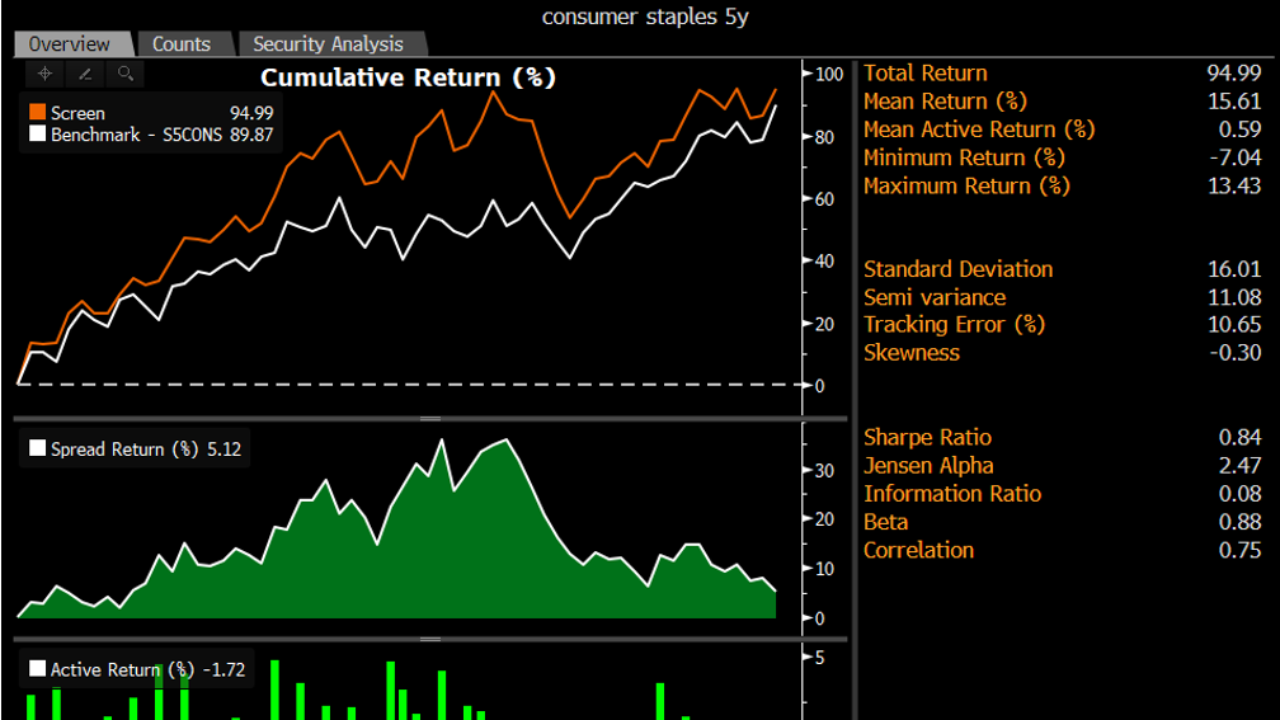

A sample rebalance following the CAN SLIM system for May 19 2026 - the most recent rebalance. See below the passing stocks and return and risk interpretation going back to 1999 and compared to the overall U.S. stock market Sp500 - (interpretation from Chat-GPT):

This portfolio appears to be a high-momentum, tactical CAN SLIM–style strategy with active rotation and ranking logic, likely integrating:

The results show a classic “high-upside growth rotation” profile rather than a low-volatility defensive strategy.

Interpretation of the Equity Curve

The red equity curve substantially outperforms the benchmark over the full test period.

From the statistics table:

| Metric |

Strategy |

S&P 500 |

| Total Return |

7,346% |

866% |

| Annualized Return |

17.06% |

8.64% |

| Max Drawdown |

-54.91% |

-55.19% |

| Sharpe Ratio |

0.72 |

0.48 |

| Sortino Ratio |

1.08 |

0.63 |

| Std Dev |

22.83% |

15.16% |

| Beta |

0.83 |

— |

| Alpha |

11.06% |

— |

Why the Higher Standard Deviation Is Acceptable

At first glance, critics may focus on:

However, standard deviation alone is often misleading for high-growth strategies because it penalizes:

That creates a major issue for growth investing.

A strategy experiencing explosive upside momentum will naturally produce:

But not all volatility is bad.

The Importance of the Sortino Ratio

The Sortino Ratio improves on the Sharpe Ratio because it isolates:

downside deviation only

rather than:

This is important because investors generally:

The strategy’s:

Sortino Ratio = 1.08

versus

S&P 500 Sortino Ratio = 0.63

suggests the portfolio generated substantially better returns relative to harmful downside volatility.

In other words:

the additional volatility appears to come disproportionately from:

rather than destructive downside instability.

Why Maximum Drawdown Matters More Here

For tactical growth systems,

maximum drawdown is often the more practical risk metric.

Why?

Because it measures:

Here:

| Metric |

Strategy |

S&P 500 |

| Max Drawdown |

-54.91% |

-55.19% |

This is extremely important.

Despite producing:

-

nearly double the annualized return,

-

and massively higher cumulative return,

the strategy experienced a drawdown profile roughly consistent with the broader U.S. equity market.

That means the system:

Interpretation of the Passing Stocks

The rebalance log shows active replacement of weakening holdings with stronger-ranked momentum names.

Stocks sold included:

-

weaker relative strength transitions,

-

deteriorating rank positions,

-

or likely failures of the momentum/technical confirmation process.

New additions included names such as:

-

IHS

-

VELO

-

SCCO

-

IMDX

-

IFS

-

TFPM

-

RDNW

-

SLGL

-

BWMX

while several stronger holdings remained:

-

ELA

-

BWV

-

AMX

-

CGEN

-

NEXA

-

XMAX

This suggests the model is operating as a:

What the Rebalance Suggests About the Strategy Logic

The rebalance behavior implies:

-

stocks are continuously ranked,

-

lower-ranked names are removed,

-

capital rotates into improving momentum candidates,

-

and technical persistence is rewarded.

The turnover (~60%) confirms the strategy is:

This is consistent with:

Risk Interpretation

This is not a low-volatility strategy.

It is a:

high-upside tactical growth strategy

designed to:

-

maximize asymmetrical upside participation,

-

while maintaining drawdown behavior comparable to the broad market.

The key evidence supporting that interpretation is:

-

higher Sortino ratio,

-

higher Sharpe ratio,

-

lower beta than expected (0.83),

-

and maximum drawdown nearly identical to the S&P 500 despite vastly higher returns.

That combination suggests:

the strategy historically generated superior upside capture efficiency rather than simply taking reckless downside risk.

Overall Interpretation

The portfolio appears to demonstrate:

-

successful long-term momentum capture,

-

tactical rotation into market leadership,

-

effective replacement of deteriorating holdings,

-

and strong upside asymmetry.

The most important statistical takeaway is likely:

The strategy generated materially higher compounded returns without materially worsening maximum drawdown relative to the S&P 500, while the elevated standard deviation appears largely attributable to upside volatility — reflected in the stronger Sortino Ratio.

The stocks are from the NYSE (New York Stock Exchange) AMEX (American Mercantile Exchange). The SP500 portfolios are on https://www.drmattlutey.com/store

Back to top